Rumor: Amazon will introduce more BNPL options

Source: November 2021, The Financial Brand

Why it’s interesting: Amazon’s new partnership with PayPal’s mobile payment service Venmo will allow users to pay for their purchases using their Venmo account. The deal could also open doors to Amazon providing additional BNPL products at checkout, considering PayPal also offers a Pay in 4 service. Although Amazon already has a partnership with Affirm, The Financial Brand notes that many online retailers provide several BNPL options at checkout.

Rumor: Amazon’s banking ambitions post-Bezos will grow.

Source: The Financial Brand

Why it’s interesting: Jeff Bezos has been a driving force behind many of Amazon’s key initiatives. It comes as no surprise that his transition to the role of executive chairman and the appointment of Andy Jassy as the new CEO raises lots of questions. For one, financial organizations wonder what Amazon’s future banking ambitions are.

Jim Marous, an expert on the digitalization of banking, says that “the decision by Bezos to step down from his current position will most likely only strengthen the commitment to financial services by Amazon.” Also, Jassy worked with Capital One, Stripe, Robinhood, and various other financial companies while leading AWS. And this experience may prove to be invaluable in helping Amazon innovate in the finance field.

Alyson Clarke, the principal analyst at Forrester, also points out that Amazon is likely to continue partnering with other financial institutions. She doesn’t think that “Amazon will — or needs to — get a license and become a bank. Any ambitions they have can be done via partnerships.”

Rumor: Amazon is building a digital currency

Source: Coindesk

Why it’s interesting: Several job postings revealed that Amazon is assembling a team to work on a digital currency project in Mexico. One job posting noted that the product Amazon is about to build will “enable customers to convert their cash into digital currency” and then use that currency to shop for goods and services, including Prime Video.

Amazon’s Digital and Emerging Payments (DEP) division is in charge of this payment product. Another job posting said that the currency is geared toward emerging markets. It remains unclear what the value proposition of Amazon-owned currency is and whether it is blockchain-based.

Perhaps the currency could be used to send money abroad to friends and family to buy specific products from Amazon’s stores. Whatever the case, Amazon has once again shown its willingness to experiment with different technologies.

In July 2021, Amazon put up another job advertisement for a blockchain and digital currency expert who would use their “domain expertise in Blockchain, Distributed Ledger, Central Bank Digital Currencies and Cryptocurrency to develop the case for the capabilities which should be developed, drive overall vision and product strategy, and gain leadership buy-in and investment for new capabilities.” The expert would join the company’s payments team. Although Amazon has yet to announce a digital currency expert as of 2022, the job posting proves it’s exploring crypto behind the scenes.

Rumor: Amazon is going deeper into the home

Source: July 2019, NY Times

Why it’s interesting: Amazon has previously worked with residential real estate brokerage Realogy to create TurnKey, a service to connect buyers and realtors on Amazon’s marketplace. However, the partnership between Amazon and Realogy was suspended in mid-2020 because of the Covid-19 pandemic. Realogy CEO Ryan Schneider said that “home services that require people being in someone’s home just doesn’t work in a Covid-kind of social distancing world.”

Nevertheless, Amazon is trying to wedge itself deeper into the home. By getting ahead of buyers as they start their search and incentivizing them with Amazon services, the company is aiming to create a massive cross-selling opportunity for its products.

It’s also a new way to grow distribution for its portfolio of home hardware devices such as Ring, smart devices like Alexa, and services like Amazon Home Services installation. The move could also help Amazon expand into home insurance or mortgage offerings.

Further reading: It’s Not Just Your Smart Speaker. How Amazon Is Coming For The $50T+ Commercial and Residential Real Estate Industries

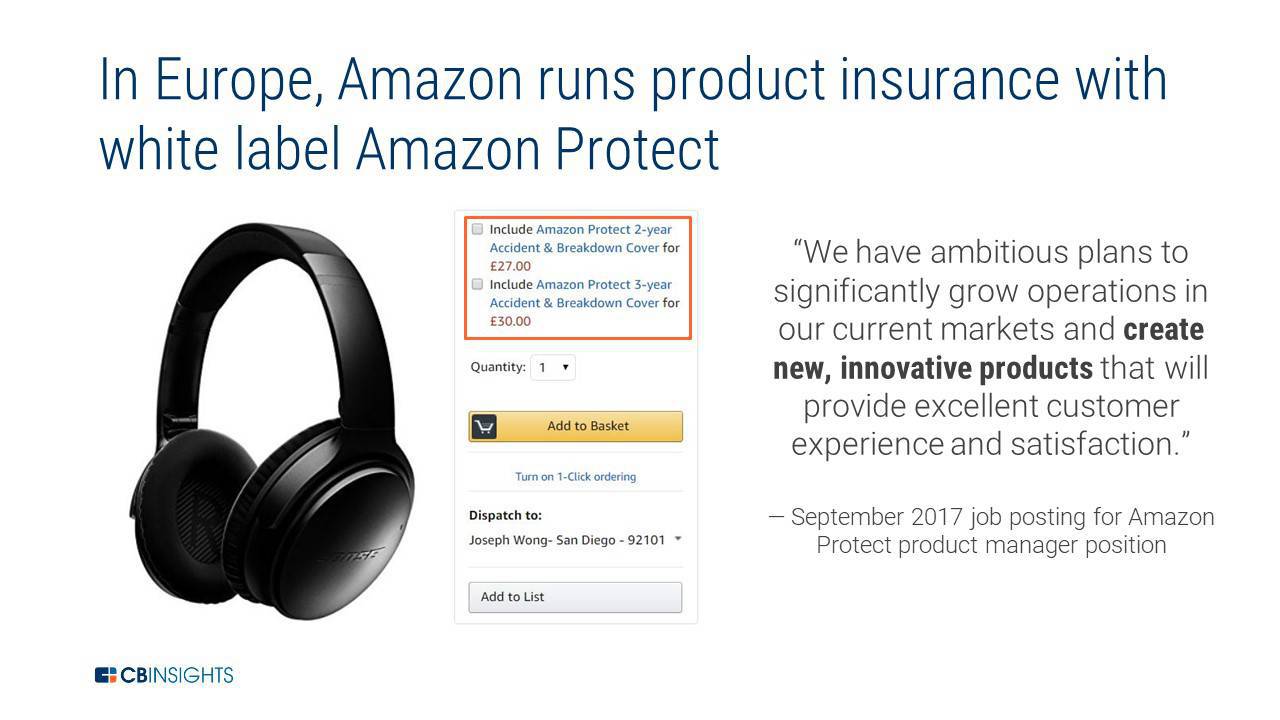

Rumor: Amazon reportedly had discussions about offering home insurance

Source: June 2018, The Information

Why it’s interesting: This rumor is based on an anonymous source that reported Amazon had discussions about offering insurance in conjunction with its connected home devices. However, none of Amazon’s existing investments or products tie to home insurance, at least in the US. While the company has made insurtech investments in India (such as in Acko) and a partnership in the EU to offer Amazon Protect, acting as more than a distributor of existing home insurance products seems unlikely.

Rumor: Amazon is getting into mortgages

Source: March 2018, Housing Wire

Why it’s interesting: While Amazon has not made concrete plans, it has been making a series of strategic hires for lending with a focus on mortgage banking. The company hired a head of its newly formed mortgage lending division. In addition, the firm has a number of home services businesses such as Alexa, Prime streaming, and Amazon Fire Stick, and this could be its next move in owning the home.

Rumor: Ripple is helping Amazon with cross border payments

Source: May 2018, CryptoDaily

Why it’s interesting: While cryptocurrencies saw a huge spike in interest in 2017, many of the world’s most prominent figures in financial services — including JPMorgan Chase CEO Jamie Dimon and Berkshire Hathaway CEO Warren Buffett — have outwardly cast it aside as mass speculation.

Amazon is known to take unconventional approaches to solve customer pain points, so it would not be surprising if it were to explore applications of blockchain across financial services products.

Rumor: Amazon and PayPal are meeting with bank regulators to expand their financial services

Source: December 2017, American Banker

Why it’s interesting: Amazon and some other FAMGA (Facebook, Amazon, Microsoft, Google, Apple) members have been making headlines with rumors of moving deeper into financial services. Skeptics have punted back that the complexity of the regulatory landscape would inhibit them from entering the market. News that the firms are connecting with financial regulators suggests that regulations are not an inhibitor, but rather just an obstacle, and meeting with the Office of the Comptroller of the Currency (OCC) is one way to get the conversation going to overcome it.

Following this meeting, the OCC worked on a fintech charter for tech firms, including Amazon, which was supposed to include a centralized application that would give tech firms a limited (but universal) financial license vs. having to go state by state for approval. However, a federal court ruled in October 2019 that the OCC did not have the authority to issue such a charter. The OCC plans to appeal the decision.

Rumor: Amazon is buying Capital One

Source: February 2017, American Banker

Why it’s interesting: This rumor was one of the earliest that suggested Amazon would buy a bank. Amazon has a decent amount of cash on its balance sheet and could use that cash to buy a small regional bank. Capital One, in particular, is already operating on the AWS cloud and is looking to make further inroads into personal finance, so it could be a good combination.

The registration flow is represented by steps 1~3 for both cases.

The registration flow is represented by steps 1~3 for both cases. When you click the “Pay” button on your phone, the basic payment flow starts. Here are the differences:

𝐀𝐩𝐩𝐥𝐞 𝐏𝐚𝐲: For iPhone, the e-commerce server passes the DAN to the bank.

When you click the “Pay” button on your phone, the basic payment flow starts. Here are the differences:

𝐀𝐩𝐩𝐥𝐞 𝐏𝐚𝐲: For iPhone, the e-commerce server passes the DAN to the bank. Over to you: Apple needs to discuss the DAN details with banks. It takes time and effort, but the benefit is that the credit card info is on the public network only once.

Over to you: Apple needs to discuss the DAN details with banks. It takes time and effort, but the benefit is that the credit card info is on the public network only once.