ONE OF THE BEST ARTICLE WHICH I COME ACROSS

2018 is going to be the year that permanently changes the way we see, and the way we use banks. Banks in their traditional form are going to start to disappear, and be replaced by what is known as banking technology – which is a completely different beast.

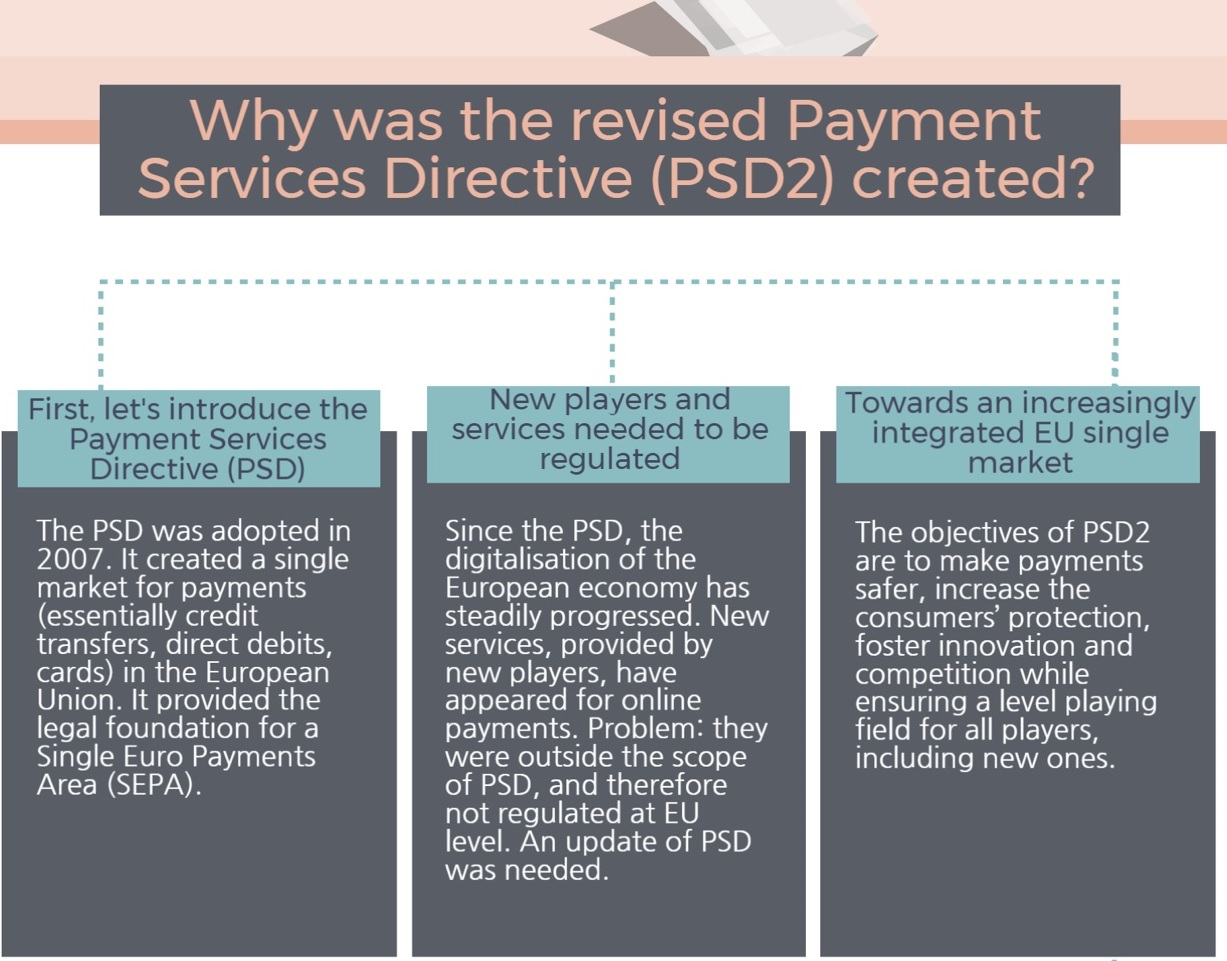

The Revised Payment Service Directive, or PSD2 as it more commonly called, is set to come into force at the beginning of next year, and “gamechanger” barely begins to describe the effect this new set of regulations governing the use of banking data will have.

PSD2 will oblige banks to give third party providers access to their customer’s accounts using Application Programming Interfaces, or APIs.

Using simple call and response technology, any firm will be able to compete tooth and nail with major banks across the same suite of services – but in the main, two new types of agent will be created.

Firstly, AISPs – Account Information Service Providers. These types of agents are service providers who have access to banks customers’ account information. This will allow them to provide customers with aggregated data from all of their various accounts, keep track of their spending, and use the data they collect to make recommendations about how best users can manage their money.

Secondly, PISPs – Payment Initiation Service Providers – PISPs are able to initiate payments on behalf of their users; allowing them to pay friends, or bills, or move money abroad, or shop at brick and mortar stores or online stores, in a wide variety of different ways.

We have already seen disruptive AISP and PISP services emerge and threaten the big banks’ hegemony over services such as Direct Debits, money transfer, customer product recommendations and real-time information (e.g. balance statements or overdraft alerts) supplied via open APIs.

But when PSD2 becomes law, the playing field will not only be levelled, it will be the banks that will be forced onto the back foot.

The banks’ labour-intensive sets of systems and controls will put them at a disadvantage when compared to smaller, more agile service providers which use only the latest technology and have no “legacy” infrastructure to replace or update.

Banks are also likely to lose the “PR War” too; their products and services have been unpopular and mistrusted ever since the global financial collapse of 2008, whereas modern fintech firms are unsullied by what has gone before and receive favourable press, as well as plenty of encouragement from their venture capitalist backers.

But it is not all bad news for banks. Firstly, they have a major advantage over the “challenger” fintech firms in that they have huge existing customer bases – they need only get their post PSD2 services right and it will be easier for them to persuade customers to stick with them rather than transfer their business to a newer, greener service.

Secondly, and somewhat ironically, some of the most successful fintech startups are, in fact, funded by the big banks. Take Atom Bank, which recently received an £83m venture round investment from Banco Bilbao Vizcaya Argentaria, BBVA, one of Spain’s biggest banks.

Or Starling Bank; run by an ex-banker, and backed by a hedge fund manager, with ex bankers and ex Financial Conduct Authority big-wigs on the board.

But from the customer’s perspective, the real difference will be experienced via the PISPs. It is the payments industry that is really set to change the face of the modern banking industry.

The biggest difference will be that payment card usage will drop – by between 9-40%, depending on your source. Eventually, payment cards may be phased out altogether.

Mobile payments, payments using wearables, payments using any Internet of Things connected devices, payments across messaging services, payments over social media. All of these services, possible already, will begin to come even more to the fore.

It isn’t hard to see big tech companies steal market share away from big banks through more agile payments services. PSD2 makes it possible for almost any firm; Apple, Facebook, even SnapChat; to act like a bank and offer the same services – but it does not work the other way.

Natwest, Santander, Barclays are not going to launch hugely popular social media platforms anytime soon – although don’t be surprised if they try – it represents their best chance of staying relevant to their invaluable Millennial customers.

But to return to the point in the title of this post, it should be customers who are most excited about this obscure regulation, PSD2, they have probably never heard of.

It gives customers’ choices galore, and significantly empowers them. For example, a merchant that pays lower fees for processing Apple Pay transactions will be desperate for customers to pay this way, and will try to entice customers to do so.

Or, challenger banks keen to wrestle customers off of big banks will offer too-good-to-be-true sign-up terms. The market for loans will become more competitive. It will become easier to open a new account. Money transfer will become fee-free and immediate.

And customers will be able to pick and choose the services they want – in effect, they will be able to construct their own banks, and maintain a transparent, real-time view of all their different accounts thanks to PSD2.

Overwhelmingly, it is the customer that has the power. They can ask any service provider, for any service, and they will get it – with bells on! They can build their own bespoke suite of services and be the masters of all the accounts they survey, chopping and changing to find the best value at the click of a mouse, or swipe of a screen. It is a future that is tantalisingly close.

And we haven’t even mentioned the blockchain and digital currencies!

The EU decided to push through PSD2 in response to the failings of the first Payments Services Directive, which many observers felt didn’t go far enough in democratising the powers of big banks.

The European Commission, via PSD2, has demonstrated that it wants to achieve 3 major goals. Improve innovation, protect customers better and make internet payments and online accounts access more secure.

But it may well be the customer who has the final word.

Huw Jenkins is CTO of The Money Cloud; Huw has been working in the FX industry, helping to accurately compare the price of sending money overseas offered by different agents and services for over 12 years. At The Money Cloud, Huw and the team are building a holistic platform from which users will be able to access all of their financial accounts, send money overseas, and apply for new products and services in just a few clicks.

2018 is going to be the year that permanently changes the way we see, and the way we use banks. Banks in their traditional form are going to start to disappear, and be replaced by what is known as banking technology – which is a completely different beast.

The Revised Payment Service Directive, or PSD2 as it more commonly called, is set to come into force at the beginning of next year, and “gamechanger” barely begins to describe the effect this new set of regulations governing the use of banking data will have.

Using simple call and response technology, any firm will be able to compete tooth and nail with major banks across the same suite of services – but in the main, two new types of agent will be created.

Firstly, AISPs – Account Information Service Providers. These types of agents are service providers who have access to banks customers’ account information. This will allow them to provide customers with aggregated data from all of their various accounts, keep track of their spending, and use the data they collect to make recommendations about how best users can manage their money.

Secondly, PISPs – Payment Initiation Service Providers – PISPs are able to initiate payments on behalf of their users; allowing them to pay friends, or bills, or move money abroad, or shop at brick and mortar stores or online stores, in a wide variety of different ways.

We have already seen disruptive AISP and PISP services emerge and threaten the big banks’ hegemony over services such as Direct Debits, money transfer, customer product recommendations and real-time information (e.g. balance statements or overdraft alerts) supplied via open APIs.

But when PSD2 becomes law, the playing field will not only be levelled, it will be the banks that will be forced onto the back foot.

The banks’ labour-intensive sets of systems and controls will put them at a disadvantage when compared to smaller, more agile service providers which use only the latest technology and have no “legacy” infrastructure to replace or update.

Banks are also likely to lose the “PR War” too; their products and services have been unpopular and mistrusted ever since the global financial collapse of 2008, whereas modern fintech firms are unsullied by what has gone before and receive favourable press, as well as plenty of encouragement from their venture capitalist backers.

But it is not all bad news for banks. Firstly, they have a major advantage over the “challenger” fintech firms in that they have huge existing customer bases – they need only get their post PSD2 services right and it will be easier for them to persuade customers to stick with them rather than transfer their business to a newer, greener service.

Secondly, and somewhat ironically, some of the most successful fintech startups are, in fact, funded by the big banks. Take Atom Bank, which recently received an £83m venture round investment from Banco Bilbao Vizcaya Argentaria, BBVA, one of Spain’s biggest banks.

Or Starling Bank; run by an ex-banker, and backed by a hedge fund manager, with ex bankers and ex Financial Conduct Authority big-wigs on the board.

But from the customer’s perspective, the real difference will be experienced via the PISPs. It is the payments industry that is really set to change the face of the modern banking industry.

The biggest difference will be that payment card usage will drop – by between 9-40%, depending on your source. Eventually, payment cards may be phased out altogether.

Mobile payments, payments using wearables, payments using any Internet of Things connected devices, payments across messaging services, payments over social media. All of these services, possible already, will begin to come even more to the fore.

It isn’t hard to see big tech companies steal market share away from big banks through more agile payments services. PSD2 makes it possible for almost any firm; Apple, Facebook, even SnapChat; to act like a bank and offer the same services – but it does not work the other way.

Natwest, Santander, Barclays are not going to launch hugely popular social media platforms anytime soon – although don’t be surprised if they try – it represents their best chance of staying relevant to their invaluable Millennial customers.

But to return to the point in the title of this post, it should be customers who are most excited about this obscure regulation, PSD2, they have probably never heard of.

It gives customers’ choices galore, and significantly empowers them. For example, a merchant that pays lower fees for processing Apple Pay transactions will be desperate for customers to pay this way, and will try to entice customers to do so.

Or, challenger banks keen to wrestle customers off of big banks will offer too-good-to-be-true sign-up terms. The market for loans will become more competitive. It will become easier to open a new account. Money transfer will become fee-free and immediate.

And customers will be able to pick and choose the services they want – in effect, they will be able to construct their own banks, and maintain a transparent, real-time view of all their different accounts thanks to PSD2.

Overwhelmingly, it is the customer that has the power. They can ask any service provider, for any service, and they will get it – with bells on! They can build their own bespoke suite of services and be the masters of all the accounts they survey, chopping and changing to find the best value at the click of a mouse, or swipe of a screen. It is a future that is tantalisingly close.

And we haven’t even mentioned the blockchain and digital currencies!

The EU decided to push through PSD2 in response to the failings of the first Payments Services Directive, which many observers felt didn’t go far enough in democratising the powers of big banks.

The European Commission, via PSD2, has demonstrated that it wants to achieve 3 major goals. Improve innovation, protect customers better and make internet payments and online accounts access more secure.

But it may well be the customer who has the final word.

Huw Jenkins is CTO of The Money Cloud; Huw has been working in the FX industry, helping to accurately compare the price of sending money overseas offered by different agents and services for over 12 years. At The Money Cloud, Huw and the team are building a holistic platform from which users will be able to access all of their financial accounts, send money overseas, and apply for new products and services in just a few clicks.

{kind=link}